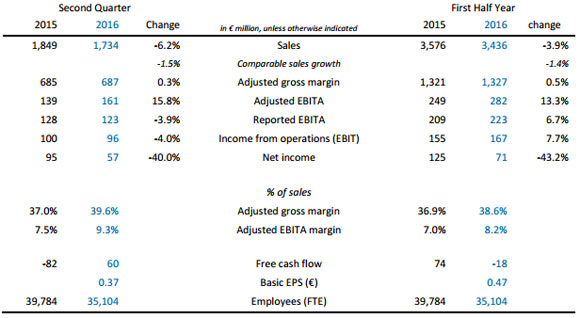

Second quarter 2016 highlights

• Total LED-based sales growth of 25%, representing 53% of total sales

• Seventh consecutive quarter of year-on-year improvement in operational profitability

o adjusted EBITA of €161 million (Q2 2015: €139 million)

o adjusted EBITA margin of 9.3% (Q2 2015: 7.5%)

• Net income of €57 million, includes separation costs and brand license fee not applicable in 2015

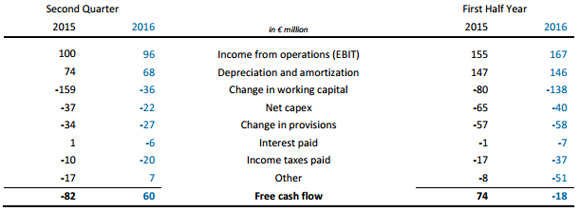

• Free cash flow of €60 million (Q2 2015: €-82 million)

Half year 2016 highlights

• Continued improvement in operational profitability

o adjusted EBITA of €282 million (HY 2015: €249 million)

o adjusted EBITA margin of 8.2% (HY 2015: 7.0%)

• Net income of €71 million, includes separation costs and brand license fee not applicable in 2015

Eindhoven, the Netherlands – Philips Lighting (Euronext Amsterdam: LIGHT) today announced second quarter and half-year results 2016. “Philips Lighting delivered satisfactory performance, posting a seventh consecutive quarter of improved operational profitability and free cash flow in the second quarter. Our businesses all progressed versus last year, performing in line with their strategic objectives,” said Eric Rondolat, CEO. “I am satisfied to see our strategy being successfully executed. The conventional Lamps Business' profitability remains well positioned despite the anticipated sales decline. Our total LED-based sales grew by 25% in the quarter and our systems and services businesses saw double-digit growth, driven by our continued extension of lighting into the Internet of Things. As a result, our LED-based activities now represent over half of total sales. We are pleased with these results, demonstrating the successful execution of our strategy. Our team remains focused on our journey of continuous improvement.”

Key figures

CFO appointment

The company also announced the appointment of Stéphane Rougeot as Chief Financial Officer, effective September 1, 2016. Mr. Rougeot succeeds Rene van Schooten, Business Group Leader Lamps, who in addition to his current role, held the position on an interim basis for nine months. Mr. Rougeot joins from Technicolor (formerly known as Thomson), where he served as Deputy CEO and President Technology Business.

Outlook

Our results in the second quarter of 2016 support our confidence that we are on the right track towards a return to positive comparable sales growth in the course of 2016. Our team remains focused on improving year-on-year operational profitability.

We expect restructuring and acquisition-related charges for the year 2016 to be in line with 1.5-2.0% of sales as previously indicated and anticipate such charges to total approximately €60 million in the third quarter, mainly driven by manufacturing footprint rationalization. In addition, separation costs are expected to total approximately €20 million for the third quarter.

Financial review

Second quarter

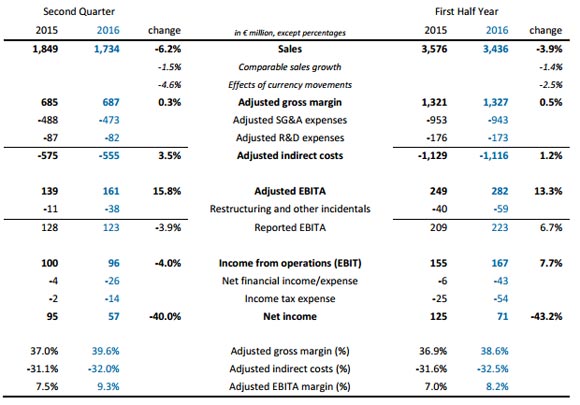

Sales amounted to €1,734 million. Comparable sales growth of -1.5% shows an improvement compared to last year, confirming Philips Lighting's path to growth. As expected, Lamps reported an increased decline versus the first quarter 2016 due to the transition from conventional to LED lighting. LED grew at double-digits, but growth slowed compared to second quarter 2015 due to a large promotion activity during the second quarter last year and lower than expected sell-out in the Americas. Comparable sales growth of Professional increased compared to second quarter 2015, driven by healthy growth in Professional North America. Home showed a double-digit comparable sales growth increase, driven by growth in both consumer luminaires and home systems.

Adjusted gross margin increased to €687 million, driven mainly by procurement and productivity savings and partly offset by price erosion. As a percentage of sales, adjusted gross margin improved to 39.6%. Adjusted indirect costs decreased to €555 million driven by cost reductions, despite the payment of a €10 million brand license fee to Royal Philips following the separation of our business earlier this year. As a percentage of sales, adjusted indirect costs increased to 32.0%. Adjusted EBITA improved to €161 million as a result of higher gross margin and lower indirect costs. Adjusted EBITA margin reached 9.3%.

Restructuring and other incidentals amounted to €38 million. Restructuring costs were €23 million, due to the shift of some restructuring activities to the third quarter 2016. Separation costs amounted to €15 million.

The decrease in net income to €57 million was primarily attributable to an increase in net finance expenses and higher income tax charges. Higher net finance expenses were related to the new financing structure of the company following its separation from Royal Philips earlier this year. Income tax expense increased by €12 million, as 2015 was favorably impacted by a one-off non-taxable income event recognized in the second quarter of that year.

First half year

Steady progress was made on overall results. Comparable sales growth of -1.4% shows an upwards trend and confirms the path to growth. Adjusted gross margin increased to €1,327 million driven by procurement and productivity savings, partly offset by price erosion. Adjusted indirect costs decreased to €1,116 million driven by cost reductions, partly offset by the payment of a €16 million brand license fee to Royal Philips. Adjusted EBITA improved to €282 million driven by higher gross margin and lower indirect costs, partly offset by unfavorable currency effects. Restructuring and other incidentals amounted to a total of €59 million. Restructuring costs were €40 million, while separation costs and acquisition-related charges amounted to €17 million and €2 million respectively. The decrease of net income to €71 million was primarily attributable to an increase of net finance expenses and a higher effective tax rate of 43.5% mainly due to non-recurring tax charges related to the separation from Royal Philips recognized in the first half of 2016.

Business highlights

- LED: Accelerating the transition to LED lighting, Philips Lighting introduced Philips CorePro LED PLC, the first LED retrofit range for compact fluorescent lamps, targeted at the professional market to replace 150 million CFLni lamps across Europe, delivering 60% energy savings. The replacement range for halogen linear lamps will be further expanded by Philips CorePro dimmable R7S LED, offering a compact form that optimally fits with existing luminaires in hotels, restaurant and cafes, enabling over 80% energy savings compared to traditional products.

- Professional / Arena: Philips Lighting expanded its stadium lighting portfolio with the installation of Africa's first Philips ArenaVision LED pitch lighting in Egypt's Cairo Stadium and is partnering with Amsterdam ArenA in the Netherlands to introduce a new combination of Philips ArenaVision LED pitch lighting with movable dynamic color spots. Philips Lighting is responsible for the pitch lighting of over 65% of stadiums involved in major international sports events.

- Professional / Public: In Rio de Janeiro, Philips Lighting completed three major public LED lighting projects, at the port area of Porto Maravilha and the highways of Arco Metropolitano and Elevado de Joá, enabling increased safety and reduced energy and maintenance costs.

- Professional / Office: Smartworld chose Philips Lighting Power over Ethernet (PoE) connected office lighting system in combination with the Cisco Digital Ceiling framework to transform its Dubai headquarters into a state-of-the-art intelligent building, enabling staff to enjoy highly personalized services that improve productivity, safety and comfort.

- Home: The Philips Hue ecosystem was strengthened by the introduction of Philips Hue White Ambiance, providing every shade of white light, and the Philips Hue 2.0 app that provides new remote control features via iOS or Android devices.

Operational performance by business group

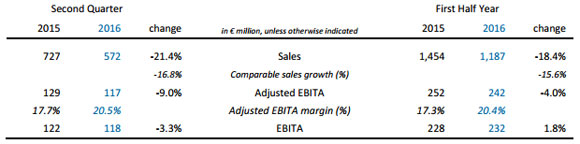

Lamps

Second quarter

Sales amounted to €572 million with comparable sales growth of -16.8%. Adjusted EBITA decreased to €117 million, while the adjusted EBITA margin improved to 20.5%. The margin increase was driven mainly by manufacturing footprint rationalization, procurement and productivity savings. During the quarter, the ceramics operation in the Netherlands was successfully divested.

First half year

Sales decreased to €1,187 million with comparable sales growth of -15.6%. Adjusted EBITA decreased to €242 million, however the adjusted EBITA margin improved to 20.4%. This was driven mainly by manufacturing footprint rationalization, procurement and productivity savings. Restructuring costs and other incidental charges in the first half amounted to €10 million, related mainly to manufacturing footprint rationalization.

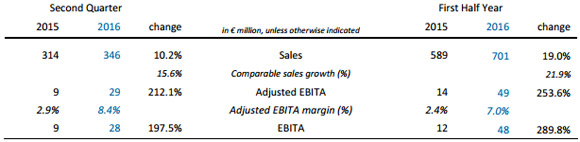

LED

Second quarter

Sales were €346 million, resulting in comparable sales growth of 15.6%. The growth rate was lower compared to 2015 due to a large promotion activity during the second quarter 2015 and lower than expected sell-out in the Americas. Other regions showed robust growth. Adjusted EBITA increased to €29 million, primarily attributable to procurement savings and operational leverage partly offset by price erosion. The adjusted EBITA margin showed a good progression at 8.4%.

First half year

Sales amounted to €701 million, resulting in robust comparable sales growth of 21.9%. Adjusted EBITA improved to €49 million driven mainly by procurement and productivity savings, and operational leverage, offset by price erosion. The adjusted EBITA margin increased to 7.0%.

Professional

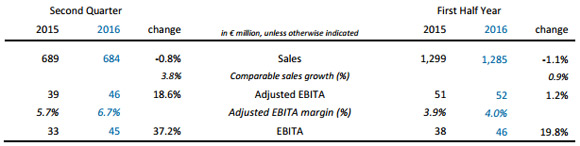

Second quarter

Sales amounted to €684 million. Comparable sales growth of 3.8% was driven mainly by growth in the Americas and the continued penetration of LED-based activities, while difficult market conditions in the Middle East & Turkey experienced in the first quarter continued to have a negative impact in the second quarter. Adjusted EBITA increased to €46 million related mainly to operational leverage and procurement savings, partly offset by write downs on bad debt in Middle East & Turkey. The adjusted EBITA margin improved to 6.7%.

First half year

Sales amounted to €1,285 million. Comparable sales growth of 0.9% was affected by difficult market conditions in the Middle East & Turkey while the North America business returned to growth. Adjusted EBITA remained stable at €52 million, despite write downs on bad debt in Middle East & Turkey. The adjusted EBITA margin was stable at 4.0%. Restructuring and other incidental charges amounted to €6 million.

Home

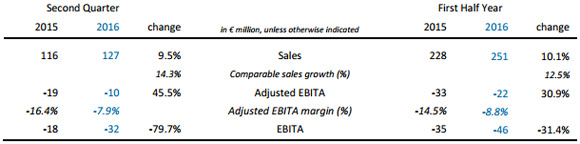

Second quarter

Sales in the second quarter increased to €127 million driven by comparable sales growth of 14.3%. Growth was supported by both the consumer luminaires and home systems businesses. All regions contributed to growth.

Adjusted EBITA loss improved to €-10 million, primarily attributable to operational leverage and procurement savings. Restructuring and other incidental charges amounted to €22 million, related mainly to the rationalization of our footprint in Belgium and China.

First half year

Sales increased to €251 million, driven by comparable sales growth of 12.5%. Adjusted EBITA loss improved to €-22 million, primarily attributable to cost reductions and operational leverage. The adjusted EBITA margin improved significantly to -8.8%. Restructuring and other incidental charges amounted to €24 million, mainly related to the rationalization of our manufacturing footprint in Belgium and China.

Other

Adjusted EBITA for other amounted to €-21 million in the quarter (Q2 2015: €-19 million) primarily originating from enabling functions, which are not reflected in the financial results of the business groups. For the first half year, adjusted EBITA amounted to €-39 million (HY 2015: €-35 million). The decrease in adjusted EBITA was primarily attributable to seasonality and phasing of costs throughout the year.

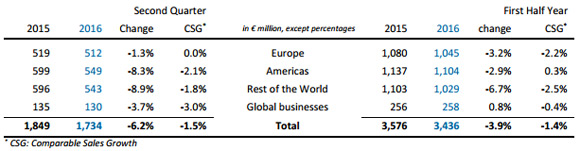

Sales by market

Financial condition

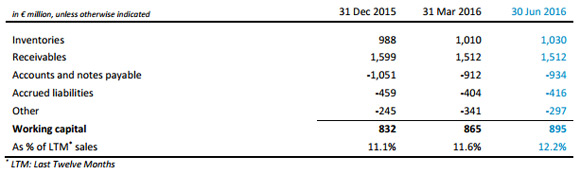

Working capital

Working capital in the first half year increased by €63 million to €895 million, mainly related to seasonal patterns within inventories, receivables and payables.

Cash flow analysis

Second quarter

Free cash flow improved to €60 million, primarily attributable to lower cash out on working capital, provisions and net capex, partly offset by increased interest payments due to a new financing structure and higher income taxes. Free cash flow in the quarter was negatively impacted by separation costs of €15 million.

First half year

Free cash flow amounted to €-18 million as the result of an increase in income from operations (EBIT) and a lower net capex level which was offset by higher working capital cash out and higher income taxes. Free cash flow in the half year was negatively impacted by €45 million for de-risking of US pensions and separation costs of €17 million.

Net debt

Second quarter

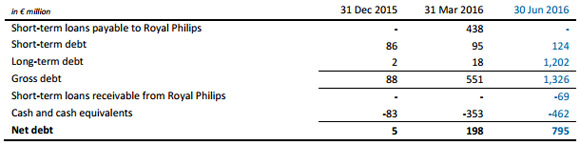

The increase of net debt to €795 million is related to the company's separation from Royal Philips and the initial public offering. In May 2016, the company raised US$500 million and €740 million through external debt facility, replacing short-term funding from Royal Philips. Group equity decreased to €2,564 million at the end of the second quarter (Q1 2016: €3,121 million), primarily in connection with the separation from Royal Philips.

First half year

The increase of net debt in the first half year is related to the separation from Royal Philips and the initial public offering in May 2016. As a result, the company now has its own financing structure, including an external debt facility of US$500 million and €740 million. At the end of June 2016, net debt amounted to €795 million. Group equity decreased to €2,564 million at the end of the first half-year (December 31, 2015: €3,616 million), primarily in connection with the separation from Royal Philips.

Other information

Appendix A – Condensed Consolidated Interim Financial Statements for the six month period ended 30 June 2016

Appendix B – Reconciliation of non-IFRS Financial Measures

Appendix C – Financial Glossary

|